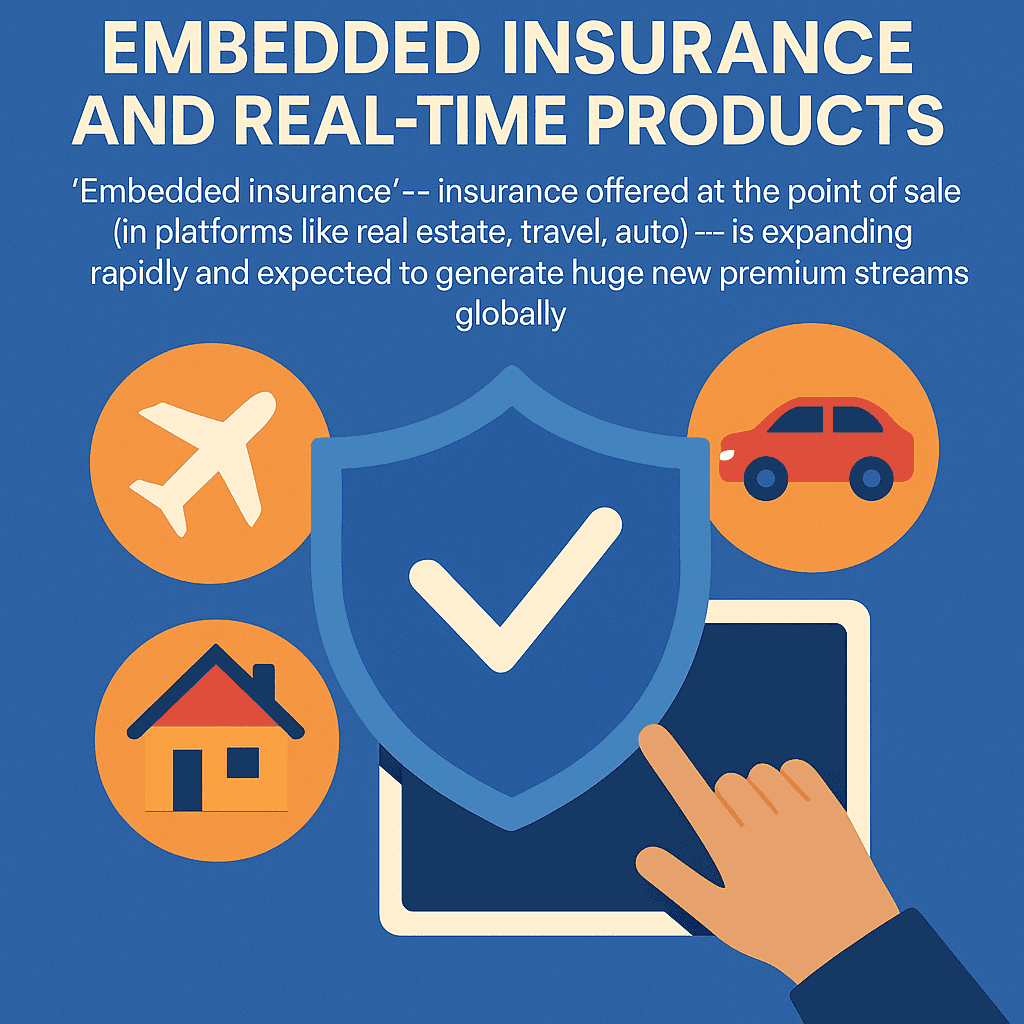

Embedded insurance is reshaping how insurance products are distributed and consumed. Here’s a more structured explanation of what it is, how it’s evolving, and why it’s generating significant buzz:

🔍 What Is Embedded Insurance?

Embedded insurance is the seamless integration of insurance products into non-insurance platforms (e.g., e-commerce, travel booking, auto sales, property platforms) at the point of need — typically during the purchase of a product or service.

🧾 Examples:

- Buying a flight and getting trip cancellation insurance offered at checkout.

- Renting a car and being offered accident coverage through the rental app.

- Purchasing a smartphone and being prompted to add theft/damage insurance.

- Buying a home and being offered homeowners insurance directly through the real estate or mortgage platform.

💹 Market Trends & Growth

- Global embedded insurance premiums are expected to surpass $700 billion by 2030.

- Digital platforms (e.g., Amazon, Uber, Airbnb) and vertical SaaS players are key enablers.

- Insurtech companies like Cover Genius, Zego, and Qover are helping legacy insurers go embedded.

🚀 Drivers of Growth

- Consumer Convenience

- Frictionless, real-time insurance at the point of transaction.

- Fewer forms, no separate insurance website visits.

- Platform Monetization

- Non-insurance companies add a revenue stream by offering insurance.

- Commissions and better customer loyalty.

- Better Risk Data

- Platforms can use behavioral or transactional data to underwrite better and personalize offers.

- Tech Enablement

- APIs and cloud infrastructure make integration simple.

- “No-code” and “low-code” tools allow faster deployment.

⚙️ Real-Time Insurance Products

This is closely related — often overlapping — with embedded insurance. Real-time insurance refers to dynamically priced and triggered policies that reflect live data.

Examples:

- Per-mile car insurance using real-time driving data.

- Gig economy insurance that activates only when the worker is on a job.

- Event-triggered travel insurance that auto-adjusts based on flight delays.

🧠 Strategic Implications

- For Insurers: They need to pivot from direct or agent-led sales to API-first, B2B2C models.

- For Platforms: Insurance is no longer just a value-added service — it can be a core monetization strategy.

- For Regulators: New models need new frameworks, especially around consent, transparency, and data use.