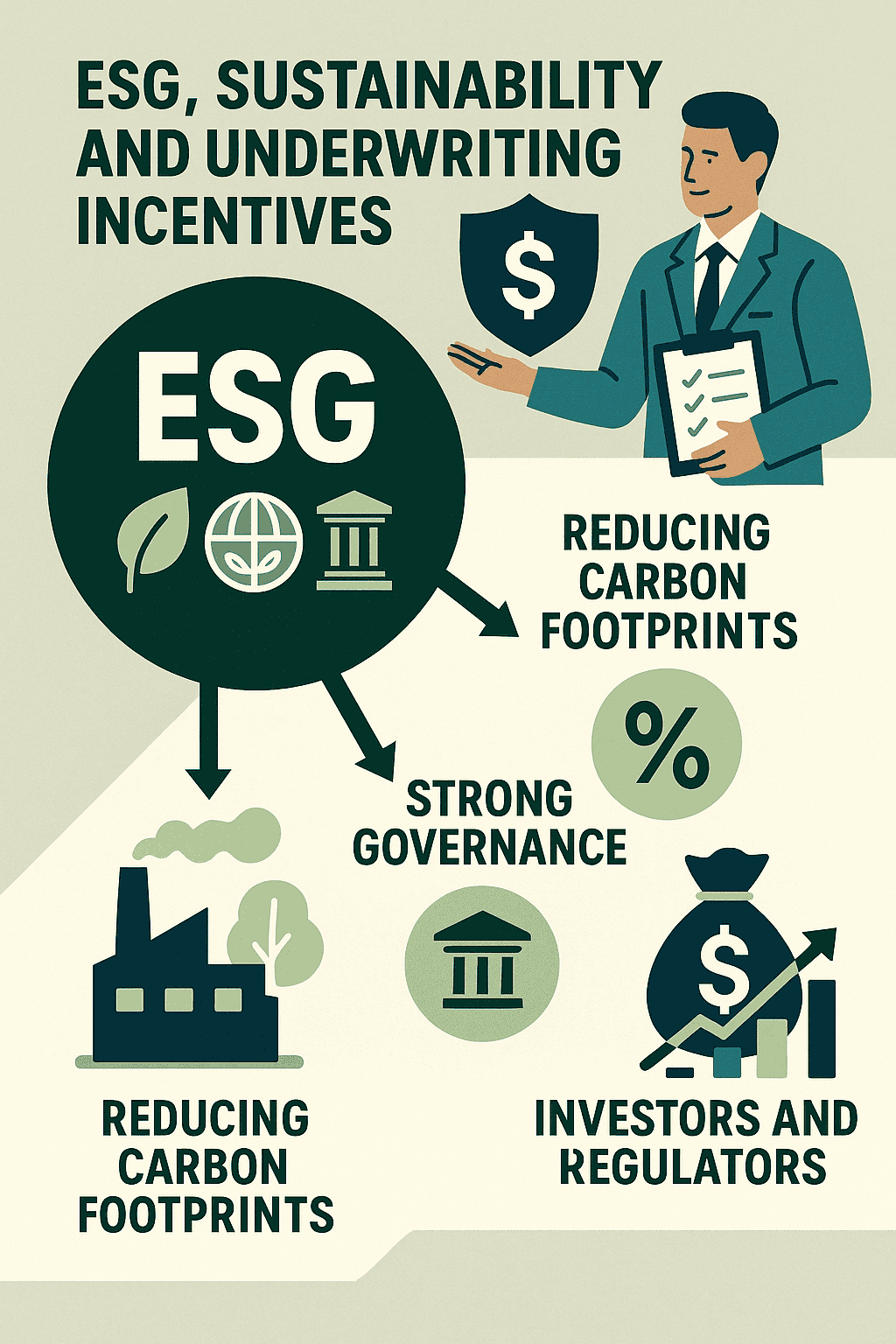

there’s been a growing trend in the insurance industry to link premiums to ESG (Environmental, Social, Governance) performance. Insurers are increasingly incorporating ESG factors into their underwriting processes and pricing models, which reflects the broader shift toward sustainability across all sectors.

How Insurers Are Linking ESG to Premiums:

- Environmental Impact (E)

- Carbon Footprints & Climate Risk: Insurers may offer discounts to businesses that take steps to reduce their carbon footprint. For example, companies investing in renewable energy, energy-efficient technologies, or carbon offset programs could see reduced premiums. Conversely, businesses with high carbon emissions may face higher premiums due to the perceived risk of climate-related damage.

- Risk Mitigation Strategies: Insurers are more inclined to offer lower rates to companies that invest in climate risk mitigation strategies (e.g., flood defenses or sustainable infrastructure), recognizing that such efforts reduce the likelihood of a claim related to climate events.

- Social Factors (S)

- Diversity & Inclusion: Businesses that actively promote diversity and inclusion, both in hiring and leadership, might be seen as lower-risk from a reputational standpoint. Insurers may reward these efforts with favorable underwriting terms.

- Employee Welfare and Safety: Companies that prioritize employee health and safety (for instance, those with strong worker’s compensation practices) may receive premium reductions.

- Governance Factors (G)

- Strong Corporate Governance: Firms with transparent governance, robust anti-corruption policies, and a strong track record in ethical business practices could be seen as less risky from an underwriting perspective, which might result in premium discounts.

- Regulatory Compliance: Companies that adhere to ESG-related regulations and standards are less likely to face fines or reputational damage, reducing the potential for costly claims or legal expenses.

The Role of Investors and Regulators:

- Investors: More investors are now demanding that companies meet ESG criteria, as they believe that companies with strong ESG practices are likely to be more sustainable in the long run. This has led insurers to align their practices with investor expectations, as it helps attract and retain investment.

- Regulators: Many jurisdictions are pushing for greater ESG disclosure from companies, and regulators are also starting to mandate that insurers incorporate ESG factors into their risk assessments. For example, the European Union has introduced regulations like the Sustainable Finance Disclosure Regulation (SFDR), which compels financial firms—including insurers—to disclose how they integrate ESG risks into their investment strategies and underwriting practices.

Incentives for Underwriting Aligned with ESG:

- Reduced Risk Exposure: By aligning with companies that take ESG factors seriously, insurers are helping to mitigate future risks (e.g., from climate change). This is because companies with strong ESG profiles tend to have lower exposure to risks like environmental disasters, social unrest, or governance-related scandals.

- Appeal to ESG-Conscious Customers: Offering ESG-aligned insurance products appeals to the growing customer base that values sustainability. Businesses that are already prioritizing ESG might be attracted to insurers that offer favorable terms based on their environmental and social responsibility.

- Long-Term Viability: Insurers themselves recognize that companies with poor ESG performance may face higher long-term risks, and those risks may increase over time as the world continues to tackle climate change, inequality, and other systemic challenges. By providing incentives for positive ESG practices, insurers are essentially future-proofing themselves.

It seems like the push for ESG-aligned underwriting is here to stay, not just because of investor and regulatory pressure, but because it aligns with long-term business sustainability. This shift offers both opportunities and challenges for insurers as they navigate risk in an evolving landscape.

Do you think the impact of ESG will continue to grow in the insurance industry, or do you see any potential pushback?