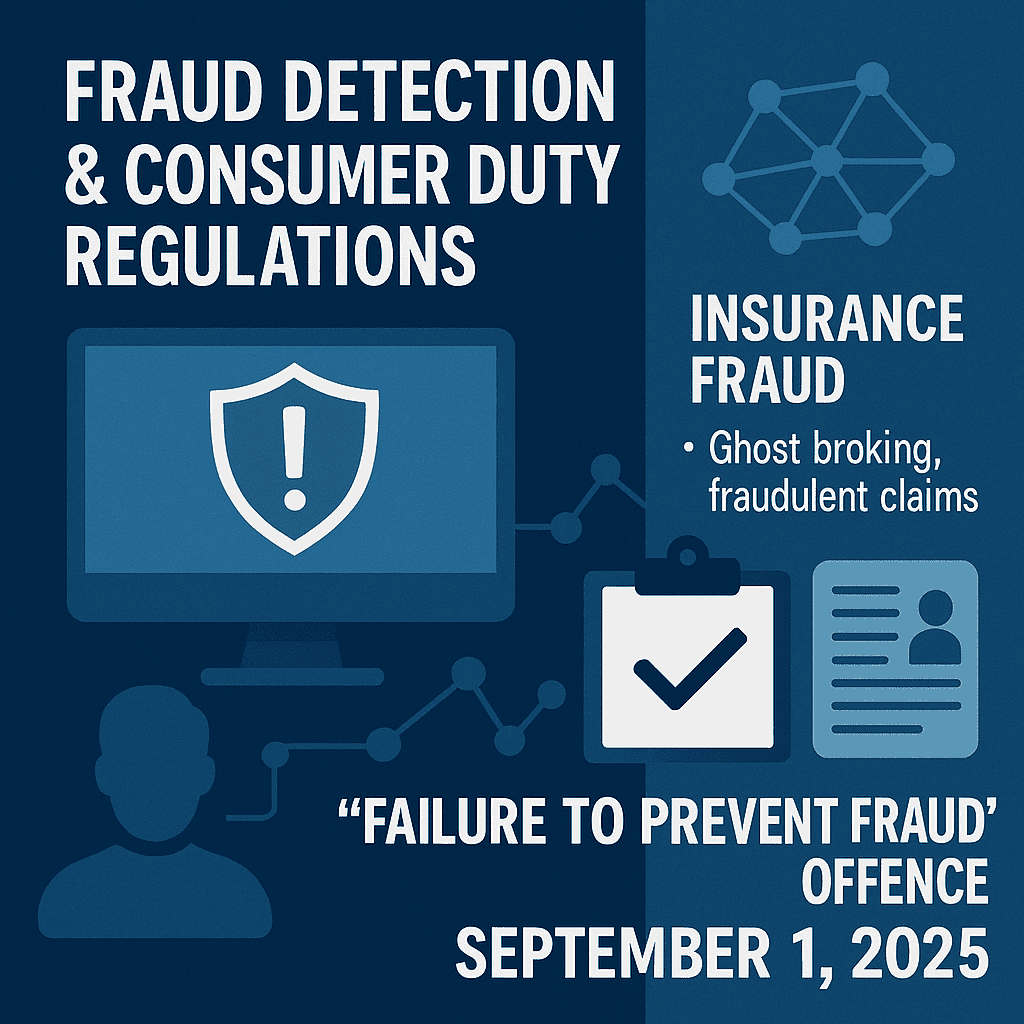

The increasing prevalence of insurance fraud, especially “ghost broking” and fraudulent claims, has sparked a greater focus on integrating customer data to combat fraud. This surge in fraudulent activities has also triggered stricter regulations, including those under Consumer Duty and the Failure to Prevent Fraud offence.

1. Insurance Fraud Types:

- Ghost Broking: This involves individuals posing as insurance brokers and offering fraudulent insurance policies to consumers. These are typically fake policies, where the consumer may pay for a non-existent or substandard cover.

- Fraudulent Claims: Policyholders who deliberately provide false information to claim more than they’re entitled to, or invent incidents to submit fake claims.

2. The Link Between Customer Data & Fraud Detection:

- Data Sharing and Analytics: Insurers are increasingly using big data, AI, and advanced analytics to detect fraudulent behavior. By connecting data across different systems, insurers can track inconsistencies, spot patterns, and identify red flags.

- Customer Profiles: Linking multiple data sources like social media, previous claim history, and identity verification services can create a more accurate and dynamic customer profile, which helps detect inconsistencies or fraudulent activities.

- Real-Time Monitoring: AI and machine learning algorithms can monitor claims and customer behaviors in real time, flagging suspicious activity as it happens, helping insurers prevent fraud before it escalates.

3. Consumer Duty Regulations:

- The Consumer Duty regulation, which came into force in July 2023, is a broad framework by the Financial Conduct Authority (FCA) aimed at improving consumer protection across financial services.

- The Core Principle of the Consumer Duty is that firms must act to deliver good outcomes for their customers. This means that businesses must:

- Identify and address fraud: Implement clear procedures to prevent fraud and ensure consumers aren’t victims of fraud (e.g., ghost broking).

- Provide clear, accurate information: Consumers should have a full understanding of their insurance products, and misleading information that could lead to fraud should be avoided.

- Manage risks of consumer harm: Insurers need to be proactive in identifying potential sources of fraud and harm, minimizing the impact on customers.

4. Failure to Prevent Fraud Offence (Effective 1st September 2025):

- This new law creates corporate liability for failing to prevent fraud. Under this offence, businesses can face significant penalties if they are found to have failed in their duty to implement systems and controls to prevent fraud, including insurance fraud.

- Key Requirements:

- Corporate Responsibility: Insurers must demonstrate that they have appropriate controls in place to detect and prevent fraudulent activities.

- Staff Training & Awareness: Businesses need to train employees on how to spot fraud and ensure that processes are in place to report suspicious activities.

- Audits & Reviews: Regular internal audits and reviews of fraud prevention mechanisms will be crucial to ensure compliance.

5. Implications for Insurers:

- Increased Compliance Burden: Insurers will need to allocate more resources to comply with both Consumer Duty regulations and the Failure to Prevent Fraud offence. This includes enhancing fraud detection systems, improving training, and ensuring thorough internal controls.

- Reputation Management: Failure to prevent fraud could not only lead to legal and financial penalties but also significantly damage an insurer’s reputation. Customers are becoming more aware of fraud risks, and an insurer’s ability to prevent fraud can be a key factor in choosing a provider.

- Consumer Protection: A major benefit of these regulations is that they aim to protect consumers by reducing fraud and ensuring that claims are processed fairly and transparently.

6. The Role of Technology in Compliance:

- Machine Learning & AI: As fraud detection increasingly leans on tech, machine learning models can help identify patterns of behavior indicative of fraud, improving accuracy and reducing human error.

- Blockchain: In the long term, blockchain technology could play a role in providing a secure, transparent, and tamper-proof method of tracking policies and claims, further reducing the risk of fraudulent activities.

- Data Privacy & Security: As insurers collect more data to detect fraud, ensuring customer data is kept secure and private is vital. Regulations around data privacy, such as the GDPR, will also play a significant role in shaping how insurers manage and process data.

Moving Forward:

Insurance companies will need to invest in robust systems and processes to stay ahead of fraud risks while adhering to regulatory changes like Consumer Duty and the Failure to Prevent Fraud offence. By leveraging advanced data analytics, AI, and maintaining a strong compliance framework, insurers can minimize the impact of fraud and protect both their business and their customers.

Do you think these changes will significantly reshape the insurance industry, or are some of these practices already in place?